How Soon After I Pay Off Mu Tsp Loan Can I Borrow Again

Recently, Michael Kitces published an article titled, "Why Paying Yourself 5% Interest On A 401(k) Loan Is A Bad Investment." My first thought was, "If information technology's a bad idea for a 401(k) loan, it must be even worse for Austerity Savings Program loans." Subsequently all, the interest on a TSP loan is nowhere virtually 5%…information technology'south tied to the G-Fund interest rate. At the time of this writing, that would be 2.25%. In other words, that's less than than half of the 401(k) loan mentioned in Kitces' commodity.

But that's not why I wrote this article. After all, I didn't know whether people actually took out TSP loans. As a affair of fact, they do. According to Government Executive, TSP participants took out more in loans in 2015 than in 2014: $four billion compared to $2.9 billion. In comparison, TSP participants took age-based withdrawals of $ii.2 billion and $2.ane billion, respectively. Age-based withdrawals are ones that you can brand later on 59 ½ without early withdrawal penalty. In other words, TSP participants took out more in loans than they did in withdrawals aligned with the typical retirement strategy.

This discovery led me to these two questions:

- "Why would someone have a TSP loan?"

- Are there whatsoever situations in which a TSP loan would make sense?

That's what this article is well-nigh. Only showtime, some TSP loan basics.

Thrift Savings Plan Loan Basics

In order to understand this, nosotros need to better empathize more about TSP loans. Below are some fundamental details.

How much tin you infringe? A TSP loan is when you take money from your TSP account for personal utilise. The loan amount tin range from $ane,000 to $fifty,000, but cannot exceed:

- Your contributions & earnings on those contributions

- The greater of $10,000 or 50% of your vested account balance (minus whatever outstanding loan rest)

- $50,000 minus your highest outstanding loan residual (at any point within the past 12 months)

Types of loans: A general purpose loan requires no documentation. However, you must repay the loan within 5 years. For a residential loan, you must provide supporting documentation. This is to verify that the proceeds will exist used for the purchase or construction of a primary residence. In this case, you can amortize the loan over a 15-year menses. For either type of loan, payments must start within threescore days of the loan disbursement.

Interest: Interest is calculated as the interest rate of the One thousand-fund at the time the loan is processed. Equally of August 2017, this was 2.25%. TSP loan payments are non tax deductible. Even so, the interest paid goes dorsum into your TSP account.

Fees: All loans require a $50 administrative fee. This is taken direct from the loan proceeds. For example, a $10,000 TSP loan will effect in net proceeds of $nine,950. However, the loan will still be for $x,000.

Loan Eligibility Requirements: The following are requirements for any TSP loan, whether it's a general purpose loan or residential:

- Must be employed past the Federal Regime or a member of the uniformed services.

- Must be in pay status because repayments are set up equally payroll deductions.

- Can only have one outstanding general purpose loan and 1 outstanding residential loan from whatsoever 1 TSP account at a fourth dimension.

- Must accept at to the lowest degree $1,000 of your own contributions and earnings in your TSP account (agency contributions and earnings cannot exist borrowed).

- Must not have repaid a TSP loan of the same type in full within the past 60 days. (If y'all have both a civilian TSP account and a uniformed services TSP account, the sixty-24-hour interval waiting period applies separately to each account.)

- Must not have had a taxable distribution of a loan within the by 12 months unless it was the result of your separation from Federal service.

- Must non have a court club against your TSP business relationship.

For residential loans, the post-obit additional requirements must be met:

A residential loan can only exist used for purchasing or constructing a master residence, which may be any of the following:

- House

- Townhouse

- Condominium

- Shares in a cooperative housing corporation

- Boat

- Mobile home

- Recreational vehicle

A residential loan cannot exist used for:

- Refinancing or prepaying an existing mortgage

- Construction of an addition to an existing residence

- Renovations to an existing residence

- Buying out another person's share in the borrower'southward current residence

- The purchase of land only

The borrower's primary residence must be purchased in whole or in part by you lot, or your spouse, if you are married.

Why would someone take a TSP loan?

There are probably a lot of reasons someone would take a TSP loan. Even so, we'll focus on the two reasons that are probably near common:

- The borrower needs the money.

- The borrower thinks there's a improve use for the money than to leave it in TSP investments.

Let'southward await at each of those a lilliputian more closely.

TSP Loan Reason #1: The borrower needs the money.

This could very well be a legitimate reason. This is particularly true if there are pressing needs and no other possible source of funds. However, even the TSP loan document warns the borrower about the touch that a TSP loan has on retirement savings. Why? There are probably a couple of reasons. Let's focus on 2:

- The borrower has no other reasonable way to borrow money.

- The borrower believes that a TSP loan is better than their other alternatives (home equity line of credit, refinance, etc.).

For the purposes of this commodity, we'll imagine a state of affairs in which there is a perfectly acceptable reason to borrow money. For case, a 'triple whammy,' like losing your spouse while transitioning from the military & having to pay for medical costs & respite care…that might be considered perfectly acceptable. Of class, each reader should accept their thought about what is considered 'perfectly reasonable.'

However, our concern is whether a TSP loan is the correct source of capital, not whether the borrower should exist taking out a loan.

Under Scenario 1, if at that place are no other reasonable ways to borrow money (outside of consumer debt, credit cards, TSP hardship withdrawal, and other high-interest forms of debt), and then the determination is simple: Exercise I borrow (or not borrow) confronting my TSP account for this purpose? In the above example, you could reasonably argue that a TSP loan makes sense, particularly if you've already gone through your emergency savings to pay for unexpected medical bills.

Under Scenario 2, y'all might have to compare the TSP loan confronting another class of debt, such as a home equity line of credit (HELOC) or a home disinterestedness loan. For simplicity's sake, we'll compare a TSP loan confronting a domicile equity loan, which has a fixed rate for the loan's duration.

In order to decide which is the better interest charge per unit, you would take to compare the home equity loan confronting the TSP loan. That should be piece of cake, right? Just figure out the G-fund'due south interest rate, and that should be what you lot're paying in interest. And since you're paying yourself interest, it'south a wash, right?

Not so fast. Kitces' article states that the 'constructive rate' is really the opportunity cost, or the growth rate of the money that you borrow, had it stayed in the original account. In other words, if you've borrowed coin that would accept otherwise been invested in the I-fund, S-fund, or C-fund, then your effective borrowing rate is the difference between the G-fund and that of those funds for the loan's period.

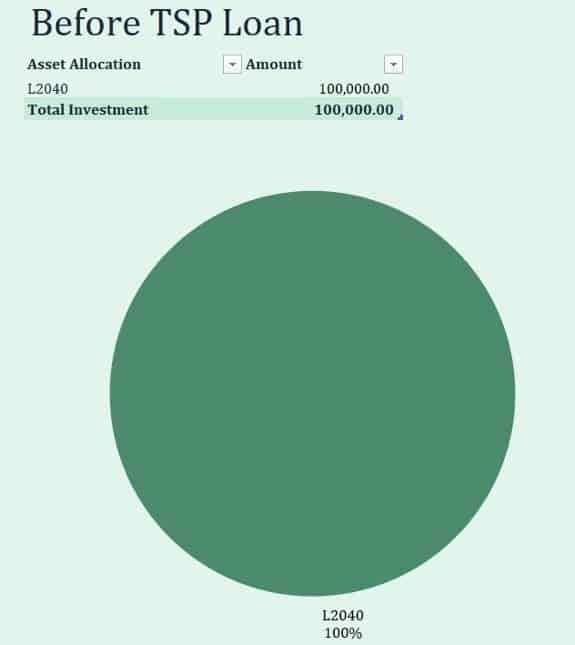

Example: Allow's think about it. Imagine a very simple TSP scenario. 5 years ago, the Smiths had $100,000 in their TSP account, all of which was in the Lifecycle 2040 fund. They borrow $50,000 for a 5-year loan. As they repay their loan, they are paying themselves involvement at the G-fund'southward involvement charge per unit of ane.75% (the Chiliad-fund's annuity rate every bit of January 2013). In that case, a $l,000 loan amortized over 5 years at one.75% yields a total of $two,256 in involvement paid. Sounds good, right?

Permit's compare this to what the Smiths could have received had they remained invested in the 2040 fund. Equally of December 2016, the L2040 fund's 5-year average was 10.21%. Every bit of this writing, the year-to-date performance was roughly in line with that number, at 9.78%. For simplicity's sake, we're going to use an average annual return of x%. Had that $50,000 stayed in TSP, at a 10% average almanac return, it would have grown to $80,525 over that same timeframe.

In order to exercise that, the Smiths would have had to borrow the coin through a dwelling house equity loan, right? Bankrate states that in 2012, vi.5% was a reasonable interest rate for a home disinterestedness loan. Using that interest charge per unit equally an instance, a similar loan amortization would have resulted in a $l,000 loan costing $eight,698 in interest. To a lender, no less.

However, the Smiths would nevertheless take been better off in the second scenario. If they paid a total of $58,698, only their $50,000 grew to $80,525, they nonetheless netted $21,827, which is over $xix,500 more than if they took the TSP loan. In that location are besides a couple of observations:

- Leaving active duty. A TSP loan, just like any loan against a defined contribution pension programme, is only available while you're notwithstanding employed. If you lot separate or retire, y'all must repay the loan in full. Otherwise the IRS deems the outstanding loan residual as a taxable distribution.

- Tax treatment. TSP loan repayments are made with later-tax dollars. This differs from TSP contributions, which are pre-tax. The reason is simple: a TSP loan is not taxed (unless it becomes a taxable distribution), so the repayment is made with after-tax dollars. Conversely, interest on a abode equity loan (upwardly to $100,000 residuum) may receive preferred tax handling, peculiarly if you itemize your deductions on Schedule A of your tax return.

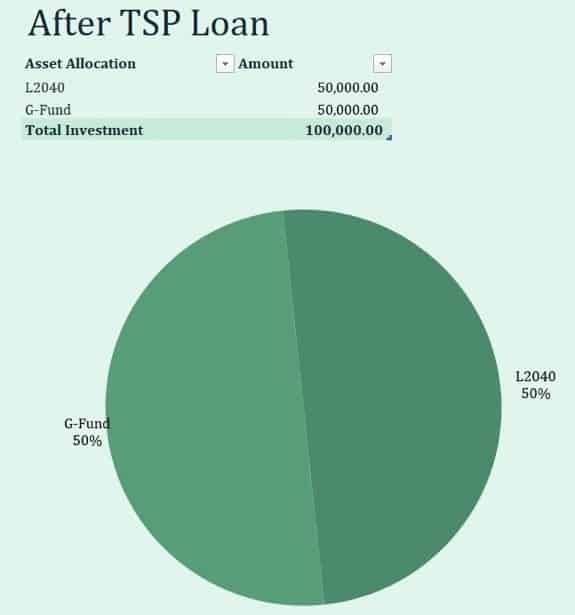

- Portfolio nugget allotment. Here is the primary touch to the Smith's investment. Prior to their loan, the Smiths had 100% of their TSP invested in their L2040 fund.

Subsequently, they substantially reduced their L2040 investment by the $fifty,000 loan, then locked themselves into the G-fund's rate of return. In other words, their asset allotment looked a lot like this:

Unless the Smiths had intended for their asset allocation to wait this way, taking a TSP loan radically inverse their investment exposure. The truest danger of a TSP loan is this:

Taking a TSP loan can dramatically alter your investment picture. Unless you account for the impact of locking in G-fund returns on your loan balance, you chance creating a portfolio that is out of sync with your investment approach.

With that said, let's look into the 2d reason someone would take a TSP loan.

TSP Loan Reason #2: The borrower believes they have a meliorate use for the money.

For purposes of this article, we're going to skip a lot of discussion nigh investment philosophy, risk, etc. We're going to focus on the utilize of TSP every bit a tax-deferred savings vehicle. We'll compare this to some normally identified uses of TSP loan proceeds (commonly identified as being what pops up on the commencement 3 pages of Google Search Results for 'investing TSP loan'). Here's what I institute:

Using a TSP Loan to Buy a Rental Property (Bigger Pockets.com). Oh boy. Nosotros tin can become downwardly a rabbit hole here. However, permit's say that you lot're a outset time rental owner. Before we determine whether a TSP loan makes sense, information technology's of import to actually make certain the purchase makes sense. Afterward all, if yous're not ready to be a landlord, then it doesn't matter where the money comes from.

Let'south assume you've run the numbers & run the scenario by all the existent estate landlording mentors that you know. They all agree: this buy is a practiced investment. If that'south the case, a bank would probably exist willing to finance the purchase. After all, a expert deal ways that the rental income will exist more than plenty to brand upwardly for all the hiccups that come along the way. And if a banking company thinks information technology's worth financing, and then why would you use your own coin to finance the deal in the get-go place? 1 of the benefits of real estate investing is the appropriate use of leverage.

If you lot keep getting turned downwardly by the bank, and then maybe the property isn't a practiced deal after all. In that example, maybe you shouldn't a TSP loan on such a risky investment. And if you can get a bank to finance the bargain, then yous tin keep your coin growing in your TSP account on a tax-deferred footing.

Tin I use TSP to invest in aureate or other precious metals? (mentioned on Zacks.com – but it's such a bad idea we're non going to link to it)

Sure. Yous can take the loan and invest in gilded, lottery tickets, tulips, or whatever you want. However, when investing in aureate, it'south important to remember a couple of things:

- Tax treatment. Gold is taxed as a collectible. Since gold doesn't pay interest or dividends, the only money you make is when you sell (assuming you sell at a profit). Collectibles are taxed at a maximum tax charge per unit of 28%. This is significantly more than long-term capital gains. Long-term capital gains are subject to a max of 20%. And forget about the taxation deferred treatment…that just exists within the retirement plan. After-tax treatment applies to TSP loan proceeds invested outside the plan.

- Liquidity. You can sell aureate relatively rapidly. In a worst case scenario, a pawn shop will give you money much faster than you lot tin can sell a house. Nonetheless, the liquidity question is, "How much value does it retain if I have to sell it chop-chop?" The immediate value of those gilt coins that William Devane sold you is the market price of their weight. That's it. Information technology doesn't thing if it's a collectible set up of coins with Thomas Jefferson, baby seals, or Thomas Jefferson clubbing baby seals, you're probably going to get less than you paid for it.

If you weren't inclined to take a agglomeration of money and buy gold with information technology, information technology's probably not a good idea to take out a TSP loan.

Taking out a TSP loan to fund Roth IRA (Bogleheads.com)

On the face of it, this seems like a pretty proficient idea. After all, you're taking a agglomeration of tax-deferred money, then using information technology to fund a Roth IRA, which is tax-free. Here are a couple of considerations:

i. Why wasn't a Roth role of your investing arroyo in the offset place? Subsequently all, TSP accounts don't grow that large overnight. If you lot're making a sudden alter just considering you want money in your Roth business relationship, y'all might want to consider why. After all, you lot're going to repay that loan with later-tax dollars, so the net result volition be fairly similar equally if you just started contributing to the Roth IRA in the first place.

However, if you're in a higher tax bracket, then foregoing the tax deferral on future TSP contributions (because you're repaying your TSP account with after-tax dollars) doesn't make sense. Y'all're essentially giving abroad your tax benefit by using after-tax coin to reimburse yourself. Just utilize the afterward-taxation contributions to fund your Roth IRA and leave your TSP to abound tax-deferred.

Conversely, if you're in a lower taxation bracket, so you might be amend off doing a Roth conversion. If you've got a means to go before separation or retirement, you might consider doing so from a traditional IRA. If you've got a lot of cash menstruum, so max out Roth TSP and a Roth IRA for both you and your spouse.

2. What are you going to invest in with the Roth IRA that you can't do inside TSP? Earlier going any farther, information technology's best to sympathize what you are going to invest in. If you're looking to diversify your portfolio, you lot might want to make sure you understand what you lot're going to diversify into. That way, yous're not just paying more money to invest in agglomeration of index funds that practice the aforementioned affair that TSP does.

However, this particular thread is interesting because of the 'unique' situation this person is in:

Due to some unanticipated expenses it is doubtful that my married woman and I will be able to max out both our traditional 401ks and Roth IRAs. I identify a higher value on fully funding the Roth since we plan to retire by the age of 50 and know that nosotros tin can withdrawal our contributions without punishment until we hit 59.five. With that said, I desire to continue to max out our 401ks because tax advantaged space should non be left on the table.

My thought is to take out a 1 year $11,000 TSP loan at 2% towards the end of the year to fully fund our Roth IRA while still maxing out our 2015 401k tax advantaged infinite.

The alternatives are to keep the money in the 401k and forfeit funding the Roth IRA this year or to significantly reduce our current TSP/401k contributions and fail to max out this year. Please explicate how either of those options is preferable to my proposal.

In other words, I don't have enough cash period to max out my contributions this year. I want to have my block and eat it as well. If that's the case, then I wonder several things:

- Volition these expenses disappear between at present and next yr? If this couple had been dutifully maxing out both accounts, and there was an emergent one-fourth dimension expense, this might make sense. However, they would have to accept the greenbacks menstruation to pay off the TSP loan and max out their investments next year.

- Is it possible to fund their Roth IRAs next year? The borderline for Roth IRA contribution is actually the taxation return due date. For 2017, the Roth IRA contribution deadline is April 17, 2018 (taxation day falls on the next business day afterwards weekends and holidays). If this couple is so cash flow positive, I'd rather meet them use the outset 4 months of the side by side year to fund their current year Roth IRA, then max out the following year's contribution.

Notwithstanding, yous can't use TSP loan proceeds to exceed the Internal Acquirement Code's IRA contribution limits. Essentially, if you take the cash menstruum to max out all your contributions, you could take a TSP loan, then repay it back. Just you'd have to put the TSP loan proceeds into an after-tax account. In that case, you'd be putting the loan proceeds into a taxable account, at the expense of your revenue enhancement-deferred savings vehicle. That doesn't make sense, either.

I might take a $30,000 401k loan simply to piss some of you off (PunchDebtintheFace.com). This is pretty funny, and really appeared college on Google rankings than the previous ii. I kept it for concluding just for the sense of humour value.

While I might non agree with the fundamentals in this article, this person seems to have plenty money set aside to afford repaying the loan. His truthful question seems to be, "What is wrong with taking a 401(1000) loan (or TSP loan, which he actually references in the article), so paying yourself the interest?

I'd say null is wrong, if that'south your fundamental approach. But so, why would you go through the trouble of doing that when the net effect is the same as taking $30,000 in your TSP and putting it into the G-fund? Either:

- Yous weren't going to invest that much coin in the 1000-fund as part of your resource allotment strategy. In that case, borrowing information technology just to pay yourself back at the Thousand-fund rate doesn't make sense.

- You were going to invest that much money in the G-fund as function of your strategy. In this scenario, it would be simpler to only continue the money in your TSP and invest that much in the G-fund.

Conclusion

Information technology appears that TSP loans exercise have a place. If you demand a loan, but don't have any options, then a TSP loan makes sense.

However, the dangers of borrowing money to earn a better investment still exist. They're actually even more than substantial than if you used a more traditional means, such equally a HELOC. Get-go, you run the risk of losing coin on your investment. Second, y'all run the run a risk of underperforming what yous would have earned had you left the money alone. Tertiary, you're jeopardizing your retirement plan on this outcome. Finally, if you aren't able to repay yourself, the loan tin can go a taxable distribution. A taxable distribution is subject to full revenue enhancement and whatever early withdrawal penalties that may utilise. Ironic, huh?

If you don't pay yourself back, you don't owe yourself… you lot owe the IRS.

So what do you think? Feel free to post your comments below.

How Soon After I Pay Off Mu Tsp Loan Can I Borrow Again

Source: https://themilitarywallet.com/tsp-loan-dangers/

0 Response to "How Soon After I Pay Off Mu Tsp Loan Can I Borrow Again"

Post a Comment